Curve x Resupply: Unlocking capital efficiency for crvUSD

The launch of Resupply has already had a notable impact on Curve’s ecosystem - driving a surge in Llamalend TVL and a sharp increase in crvUSD supply. Let’s find out what it is and how it works:

Resupply

Resupply is a decentralized stablecoin protocol that leverages the liquidity and stability of lending markets to unlock greater capital efficiency. Built on top of Curve’s lending markets, it allows stablecoins supplied to Curve’s Llamalend - such as crvUSD - to serve as productive collateral.

Resupply accepts Curve lending market receipts as collateral, enabling leveraged yield farming.

The result: increased crvUSD demand, deeper Llamalend liquidity, higher yields, and better capital efficiency.

- Resupply Team

Developed by contributors from Convex and Yearn, Resupply introduces reUSD: a decentralized stablecoin backed by Collateralized Debt Positions (CDPs), which can be borrowed against yield-bearing stablecoins like crvUSD. The protocol supports both Curve's Llamalend and Frax lending markets.

Resupply is now Officially Live! — It's time to make your stablecoins work harder for you!

— Resupply (@ResupplyFi) March 20, 2025

You can now borrow $reUSD, a decentralized stablecoin backed by yield-bearing lending vault tokens. Visit our dAPP which is now live at: https://t.co/oQPvcLNJm8 and start earning now!

1/5 pic.twitter.com/1xlOh4S4QV

Resupply enables users to borrow reUSD against their existing stablecoin positions without giving up yield. For Curve users, this means crvUSD deposited into Llamalend can continue to earn interest and CRV incentives (boosted via Convex), while simultaneously serving as collateral to mint reUSD—effectively unlocking additional liquidity from otherwise idle assets.

How it works

Users deposit crvUSD into supported lending markets on Curve. This can be done directly via the Resupply UI. Current supported markets include sDOLA, sUSDe, sfrxUSD, WETH, wstETH, USDe, and WBTC.

These deposits continue to earn lending interest and CRV incentives (boosted via Convex). At the same time, they can be used as collateral to mint reUSD, unlocking additional capital without sacrificing the underlying yield.

Borrowing costs are designed to favor capital efficiency. The interest rate is dynamically set to the greater of:

- 50% of the underlying lending rate

- 50% of the “risk-free rate” (defined as the current APY of sfrxUSD)

- 2% flat

This structure ensures borrowers typically maintain a positive yield spread. It also enables looped strategies - for example: borrowing reUSD, swapping it for more crvUSD, and redepositing - compounding exposure to Llamalend yields and maximizing returns on collateral.

For more details on how the protocol works, visit the Resupply Documentation.

Impact on Curve

Resupply enhances the utility of crvUSD by enabling it to serve as productive collateral for leveraged yield strategies. As reUSD adoption grows so does crvUSD, as it drives additional deposits into Llamalend (Curve Lend) - expanding the available supply for borrowers and contributing to more efficient, lower borrowing rates.

In short: increasing demand for crvUSD leads to more of it being borrowed, which in turn generates more revenue for veCRV holders.

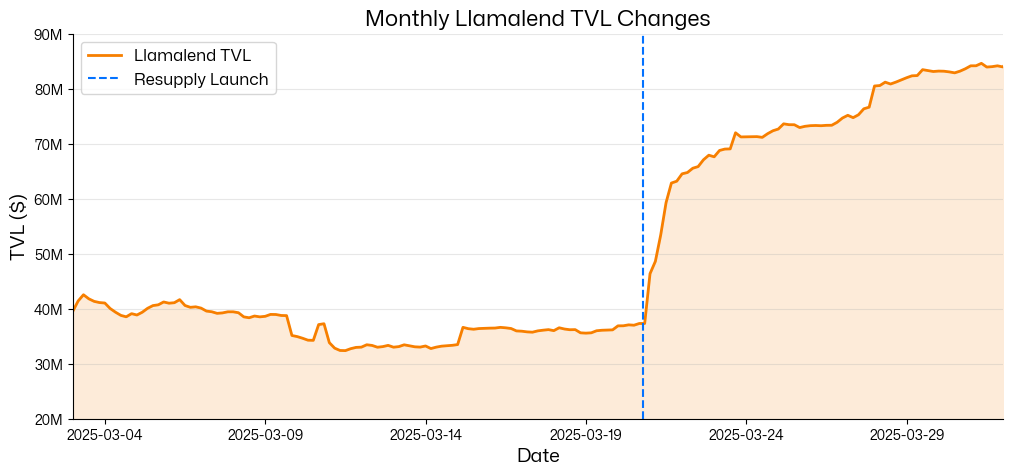

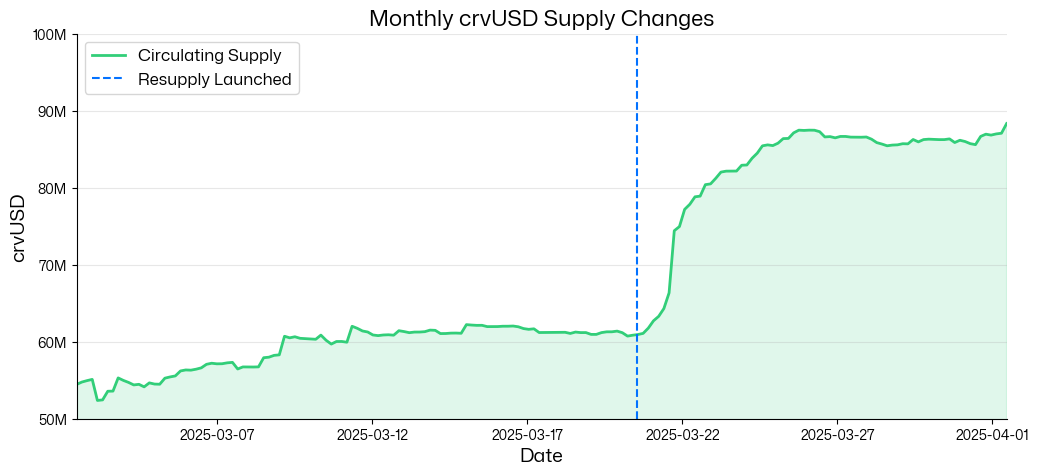

Despite launching a progressive deployment rollout just a week ago, Resupply is already showing a significant impact on both Llamalend TVL and crvUSD supply: